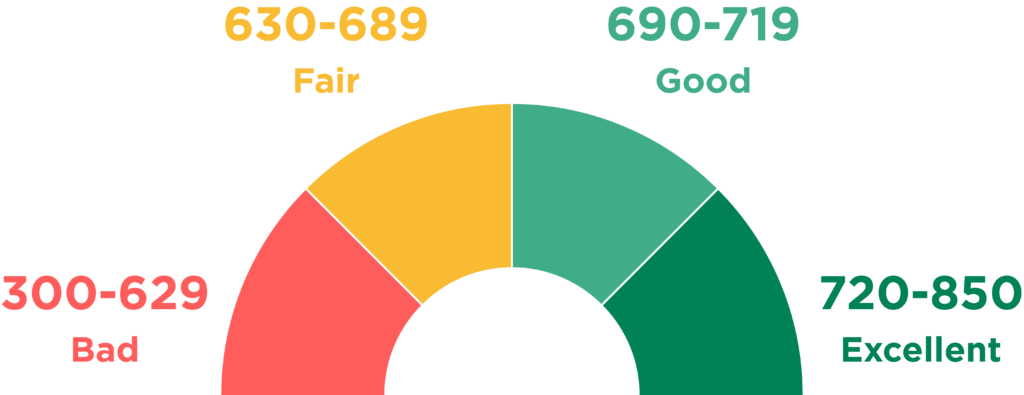

Credit Scores

Your credit history is important to a lot of people: mortgage lenders, banks, utility companies, prospective employers, and more. So it’s especially important that you understand your credit report, credit score, and the companies that compile that information, credit bureaus.

Credit scores are extremely important especially if borrowers are in the market for a home or simply applying for credit cards, personal loans or loans to send their children to college. It is important that borrowers are aware of their credit score. The higher the credit score, the better chance one has of obtaining credit with a more reasonable interest rate. When the score is lower, keep in mind – there are things that one can do to improve it over time.

Potential creditors look at credit scores to let them know whether bills are paid on time, if borrowers have defaulted on any loans and also to determine if borrowers keep their credit cards at the maximum credit line. Credit scores are looked upon as an overview. It is suggested that all consumers review their credit report and view it at least once per year.

You can get one free credit report every twelve months from each of the nationwide credit bureaus—Equifax, Experian, and TransUnion—by visiting www.annualcreditreport.com or calling (877) 322-8228.

You will need to provide certain information to access your report, such as your name, address, Social Security number, and date of birth. You can order one, two, or all three reports at the same time, or you can request these reports at various times throughout the year.

The option you choose will depend on the goal of your review. A report generated by one of the three major credit bureaus may not contain all of the information pertaining to your credit history. Therefore, if you want a complete view of your credit record at a particular moment, you should examine your report from each bureau at the same time. However, if you wish to detect any errors and monitor changes in your credit profile over time, you may wish to review a single credit report every four months.

The Different Credit Scores

Having No Credit

Having no credit means that an individual has not established a credit history with any lending institutions or credit bureaus. While it might seem like a neutral situation, it can be a bad thing in certain situations. Without a credit history, lenders have no information to assess the individual’s creditworthiness, making it challenging for them to qualify for loans or credit cards.

Without a credit history, it becomes challenging to prove financial responsibility, which can result in:

- Limited access to credit: Lenders may be hesitant to extend credit to someone without a credit history, making it difficult to secure loans or credit cards.

- Higher interest rates: If you do manage to get approved for credit, the lack of credit history may lead to higher interest rates, as lenders consider you a higher risk.

- Difficulty renting an apartment: Landlords often check credit history to evaluate potential tenants’ reliability in paying rent on time.

- Higher insurance premiums: Some insurance companies may consider credit history when determining insurance premiums.

Authorized User

Here are some tips on how to best use authorized users to build and improve credit:

- Become an authorized user on someone else’s credit card account. This is the simplest way to start building credit, as you will be piggybacking off of the primary cardholder’s good credit history.

- Make sure the primary cardholder has a long history of on-time payments and a low credit utilization ratio. These factors will have a big impact on your own credit score.

- Be responsible with your spending. Even though you are not legally responsible for the debt, you should still make all of your payments on time and in full. This will show creditors that you are trustworthy and reliable.

- Ask to be added as an authorized user on multiple credit cards. This will give you a wider credit history and help you build your credit even faster.

Here are some examples of how authorized users can help build credit:

- Let’s say you are a young adult with no credit history. If you are added as an authorized user on your parents’ credit card account, you will start building your own credit history immediately. Even if your parents only use the card for a few small purchases each month, you will still benefit from their good credit history.

- Let’s say you have a limited credit history and you are trying to improve your credit score. If you are added as an authorized user on a credit card with a high credit limit, your credit utilization ratio will go down. This is because your available credit will increase without your actual spending increasing.

Overall, authorized users can be a great way to build and improve credit. However, it is important to be responsible with your spending and to make sure that the primary cardholder has good credit history.

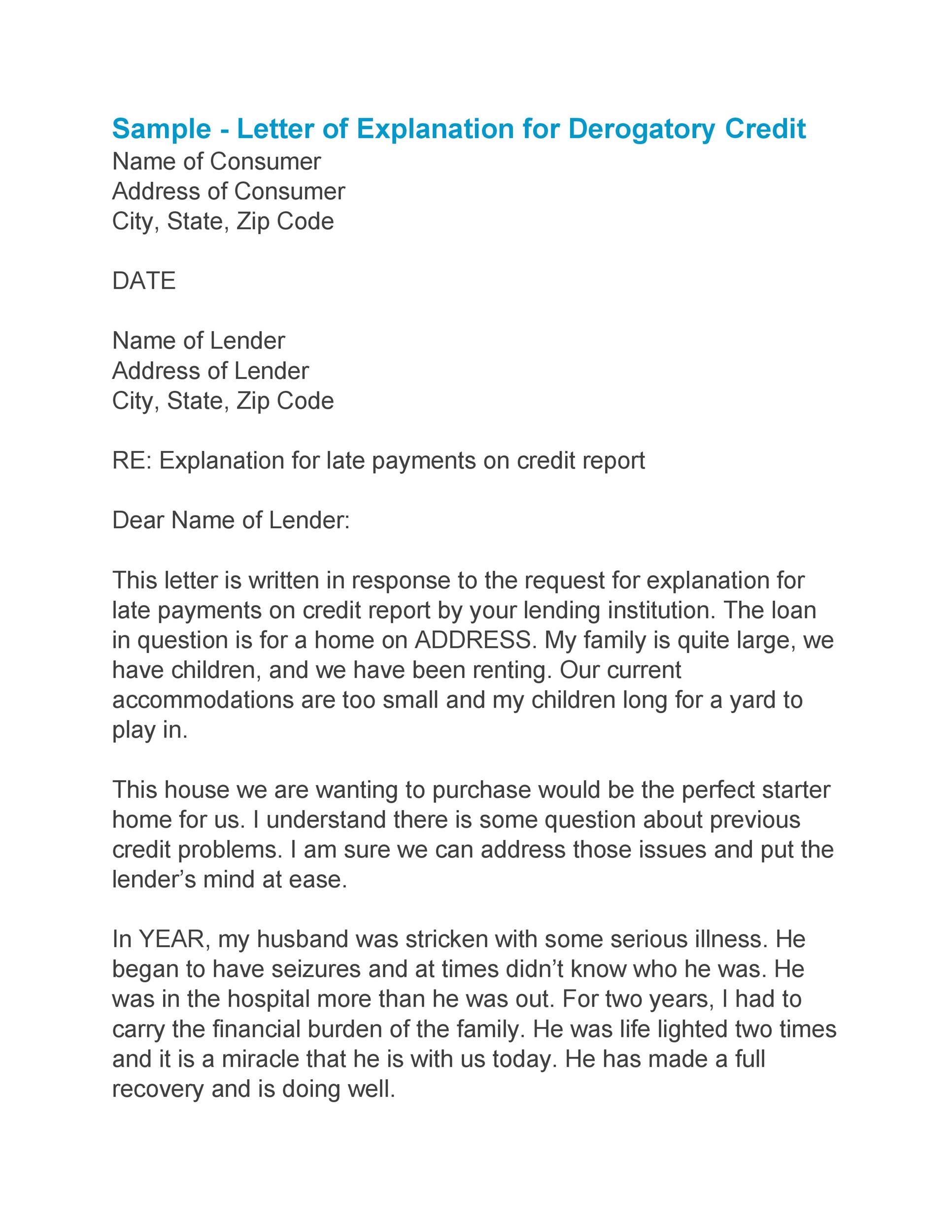

Letters of Explanation

Letters of explanation for credit, also known as credit explanation letters or LOEs, are written statements provided by individuals to explain specific negative or unusual items on their credit reports. These letters are typically submitted to lenders or creditors during the loan application process to provide context and clarification regarding certain financial events or discrepancies that may have impacted the individual’s credit history.

Common reasons for writing a letter of explanation may include:

- Late payments: Explaining the reasons behind late payments, such as unexpected financial hardships or personal circumstances.

- Medical issues: Detailing medical emergencies that led to financial difficulties and affected credit obligations.

- Identity theft or fraud: Providing an explanation if certain credit items are the result of fraudulent activities.

- Disputed items: Explaining the outcome of disputes with credit reporting agencies regarding inaccuracies or errors on the credit report.

- Short sale or foreclosure: Explaining the circumstances surrounding a short sale or foreclosure on a property.

- Bankruptcy: Clarifying the reasons for filing bankruptcy and outlining efforts made to improve financial management.

When writing a letter of explanation, it’s essential to be concise, honest, and provide any supporting documentation if available. The goal is to present a compelling case that helps lenders understand the circumstances surrounding negative credit events and to demonstrate a commitment to responsible financial behavior moving forward. A well-crafted letter may positively influence a lender’s decision-making process and improve the chances of obtaining credit or loan approval.

Conclusion

In conclusion, credit plays a pivotal role in modern financial systems, profoundly impacting our lives in various ways. A strong credit history opens doors to numerous opportunities, allowing us to secure loans, mortgages, and credit cards with favorable terms. It empowers us to make significant life decisions, such as buying a home, starting a business, or pursuing higher education.